How external carbon pricing increasingly affects freight transportation

Read this blog article to gain insights into the various carbon pricing schemes applied to different modes of transport, and why transport and logistics companies like carriers, forwarders and cargo owners should explore the opportunities available to reduce CO2 emissions.

Key Takeaways

- Carbon pricing is now showing up operationally across modes (maritime, road, air) via instruments like taxes, fuel standards (e.g., FuelEU Maritime), and trading schemes (EU ETS), and it is passed through the chain from energy suppliers → carriers → cargo owners/customers (e.g., via surcharges).

- It changes the job for both sustainability and supply chain teams: sustainability needs credible reduction strategies and investments; supply chain must optimize networks, consolidate, collaborate with lower-emission suppliers, and use tech to reduce emissions-related cost exposure.

- Surcharges introduce volatility and transparency issues – maritime EU ETS is the clearest example. Carriers apply ETS surcharges per TEU using market EUA prices, but methods and review intervals differ, creating notable price gaps between carriers and uncertainty for cargo owners. Some argue surcharges can exceed allowance-equivalent costs.

Action checklist

- Treat carbon costs as a variable cost driver: add ETS/toll surcharge scenarios into contracting and lane economics.

- Reduce exposure with “no-regrets” levers: network optimization, mode shift where feasible, load consolidation, and carrier selection based on efficiency/emissions.

- Invest in emissions visibility at shipment and lane level so you can cut emissions and carbon-cost spend simultaneously.

The transportation and logistics sector has moved into the focus of carbon pricing. This primarily stems from the fact that the industry contributes around eleven per cent to global greenhouse gas emissions. Carbon pricing emerges as a cornerstone of climate policy. Instruments like taxation, fuel standards (e.g., FuelEU maritime) or emission trading schemes such as the EU Emissions Trading System (ETS) or the Energy Taxation Directive (ETD) has pushed decarbonization targets further into the logistics sector, affecting already many companies in their daily business. Two examples:

- For sustainability managers, carbon pricing necessitates the development and implementation of comprehensive emissions reduction strategies, pushing for investments in cleaner technologies and sustainable practices to meet regulatory requirements and achieve long-term environmental goals.

- Supply chain managers must optimize logistics and supply chain processes to minimize emissions-related costs. This includes adopting efficient transportation methods, collaborating with low-emission suppliers, and leveraging innovative technologies to enhance operational efficiency.

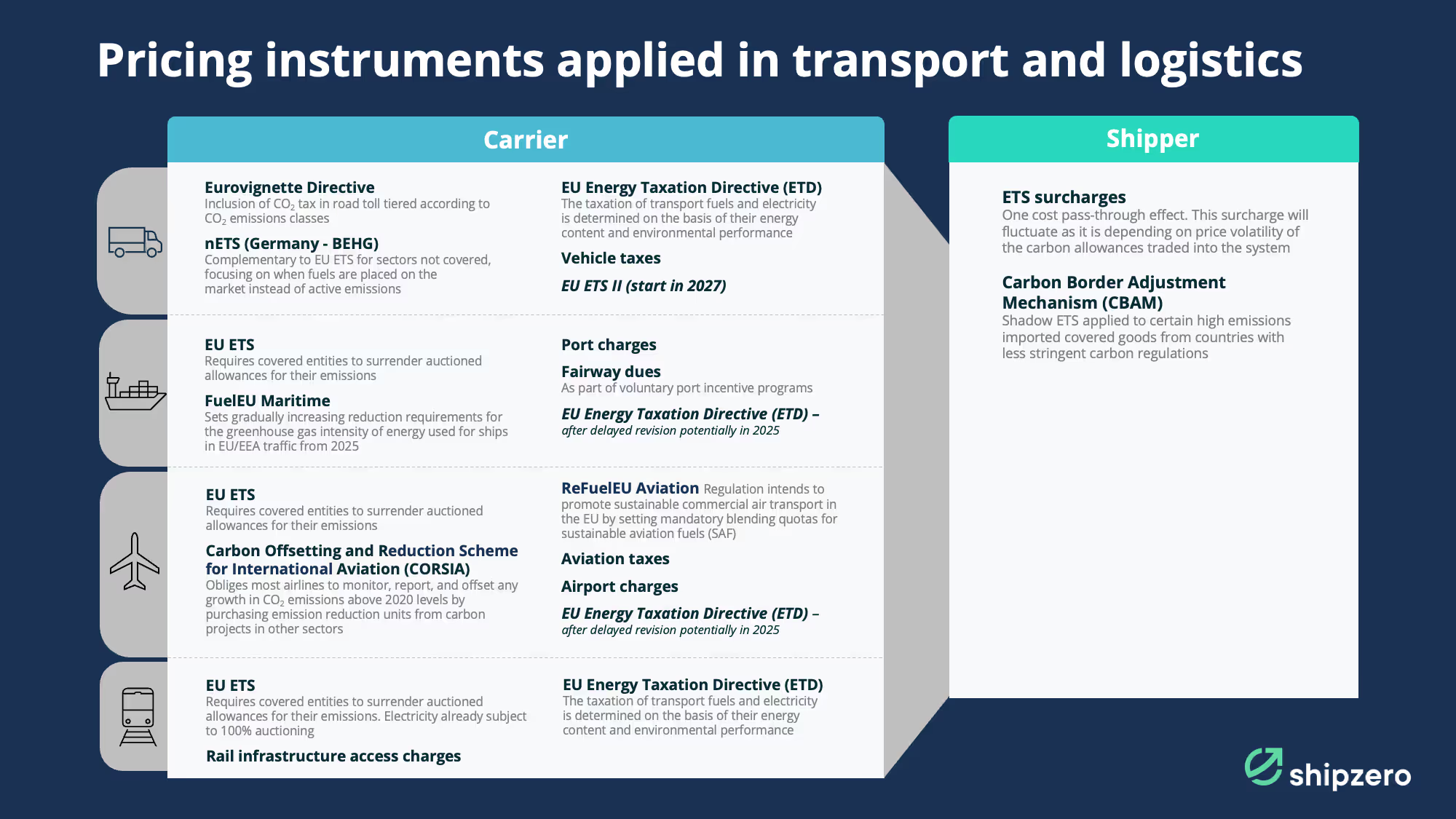

Within the industry, carbon pricing plays a crucial role in various characteristics such as ETS surcharges, CO2 tolls or fuel prices. Precise emission management is an indispensable prerequisite to fulfill all different regulatory requirements in diverse systems for various transportation modes such as maritime, road and air.

Carbon price levels, initially incurred by energy suppliers, are subsequently passed on to customers, directly or indirectly, through carriers. The integration of diverse carbon pricing mechanisms aims to create a range of incentives, fostering a multifaceted approach to emission reduction. Despite individual inconsistencies such as the current direction of the toll or the ETD, the overarching strategy is aimed at promoting sustainable fuels and drive systems and at the same time eliminating possible market inequalities that could put certain modes of transport at a disadvantage.

Carbon pricing supports energy efficiency

All these measures aim to have a positive impact on more sustainable logistics in the future by improving energy efficiency (by reducing energy demand per tonne-kilometre), using lower-carbon fuels (measured in terms of greenhouse gas emissions per unit of energy consumed) and reducing the overall demand for emission-intensive modes of transport, thus supporting the shift to low-carbon modes such as rail.

While carbon pricing can increase freight costs and consumer prices, it also offers companies the opportunity to gain a competitive advantage by effectively managing and reducing their emissions, ultimately benefiting both the environment and their bottom line. However, carbon pricing alone will not deliver deep reductions in greenhouse gas emissions and should be seen as a complement to, rather than a substitute for, ambitious fleet carbon targets and quotas.

Impacts on Market Dynamics: example of maritime shipping surcharges

The introduction of carbon pricing mechanisms significantly influences market dynamics, particularly in sectors and companies heavily reliant on fossil fuels and emission-intensive transport options. These mechanisms lead to immediate impacts on product and service costs, affecting both businesses and consumers alike.

In sectors such as maritime shipping, where the implementation of the EU Emissions Trading Scheme has prompted companies to levy ETS surcharges and pass on the additional costs throughout the logistics chain, the dynamic is most noticeable. The ETS CO2 emissions per TEU are based on methodology by the Clean Cargo Working Group, incorporating market prices for EU allowances (EUAs).

Specifically, for voyages in European waters, the CO2 calculations are multiplied by the market price for EUAs, sourced from the ICEDEU3 index using a three-month average. This enables carriers to determine and apply an ETS surcharge per TEU. The implementation of this system will occur in phases. Initially, 40% of greenhouse gas (GHG) emissions will be payable in September 2025, covering the period from January 1, 2024.

Subsequently, in 2026, carriers will be responsible for paying for 70% of emissions generated in 2025. Finally, starting from 2027, carriers will be required to cover 100% of the emissions generated in 2026 and beyond.

Yet, indicating significant uncertainty regarding the projected ETS surcharges to be imposed on cargo owners, these surcharges and respective guidance vary between companies as the price review intervals differ between monthly or quarterly.

For example, on a high-volume Asia-Europe tradelane, providers like CMA and Hapag-Lloyd show a price difference of more than 12% for dry containers. For reefers, the gap is even more pronounced, with a 30% difference per TEU prices (in euros) during Q4 2024.

Navigating price volatility

The lack of transparency regarding the methodologies used to calculate these surcharges has sparked concerns. Some argue that they may not accurately reflect the real level of costs but instead serve to increase revenues, as suggested by a recent study.

Surcharges can be two to three times higher than the equivalent current EU allowance price. This is due to different calculation methods that account for price volatility, fleet utilization and administrative costs. The limited transparency of these calculations and the complexity of the cost forecasts offer possibilities to exploit them while the market is still struggling with the uncertainties of the system. However, in the long term, competition among carriers is expected to drive more equitable and transparent pricing.

Despite the still relatively small share contributed to total transport costs, disparities in ETS surcharges are likely to perpetuate discontent among stakeholders - especially when ETS reaches 100% coverage in 2026. It's crucial to consider price fluctuations in logistics processes, which are increasingly being incorporated into contracts.

Maximize efficiency in transportation

As such, stakeholders must gear up for maximum efficiency in transportation management to mitigate additional costs in both the short and long term. Optimizing networks, using greener modes of transport where feasible, consolidating loads, and demanding greener vehicles from carriers are among the strategies to reduce greenhouse gas emissions and the need for carbon allowances.

However, decarbonizing logistics processes is complex and takes time. Hence, having visibility into emissions allows for effective reduction strategies and simultaneous decrease in emission cost.

—

Sources:

Transport & Environment: Profits uncontained – an analysis of container shipping ETS surcharges

CMA CGM: Carrier Charge Finder

.avif)